Nobody is talking about the five letter word

P-I-M-C-O. There, I wrote it. Bond flows continue to outpace equities. And PIMCO is taking a huge leap forward in market share. But the scale became evident by reading an advisor’s suggested portfolio (WSJ id/pwd required). In that article, Mr Malloon suggests investing nearly 40% of a model portfolio with PIMCO. Obviously, let’s give credit where credit is due. PIMCO is hitting on all cylinders if they’re readily convincing a long-term professional to allocate 40%.

Are executives elsewhere coming up with marketing strategies to counter-attack? What steps could be taken? Here’s a simple 4P review (product, price, promotion, place), with a focus on product.

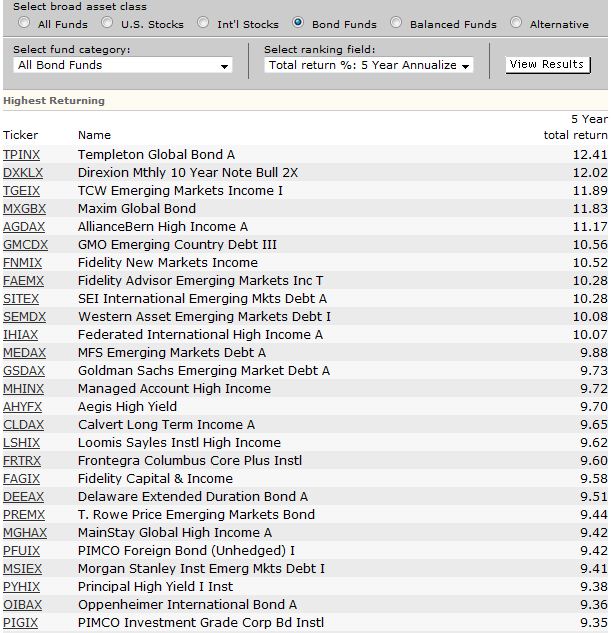

- Product – Mutual fund products are closely tied to performance and we all know – nobody can guarantee performance. Many industry insiders tie flows to performance. The conventional wisdom is that the PIMCO funds are “killing it.” Are they? Using Morningstar, PIMCO’s first fund ranks 23rd for 5-year return (see here). There are 20 fund families outperforming. Past performance is not an indicator of future performance and communications have to be careful to avoid supporting that message. Nonetheless, is there an opportunity to dispel the conventional wisdom?

- Price – Interesting idea – can a fixed income shop promote themselves as “the lower-cost way to fixed income investing?” I think so (obviously some compliance perspectives will be necessary). That’s an interesting strategy. That firm will learn: what is the sensitivity to price for fixed income? Also, how robust are the PIMCO margins – will they match the lower cost?

- Promotion – PIMCO, Bill Gross in particular, does this extremely effectively. He’s on TV. He’s in the paper. He’s podcasting. Developing a promotional platform to rival that is difficult, slow, and risky. Nothing to see here.

- Place – Potentially the best marketing opportunity is to find a channel or distribution partner that is looking to diversify AUM. Probably, there are risk managers at each wirehouse firm calculating percentage of assets in PIMCO funds and subsequently signaling the potential danger therein.

{kind=link}

There are additional considerations and approaches. The first step is to acknowledge the elephant in the room. And that the elephant is hungry. Is this the new normal?